Backtesting (External Data)

Online Link¶

Initialization: set backtest stock id and time period

import numpy as np

import pandas as pd

from FinMind import strategies

from FinMind.data import DataLoader

from FinMind.strategies.base import Strategy

from ta.momentum import StochasticOscillator

data_loader = DataLoader()

# data_loader.login_by_token(api_token='token') # optional

obj = strategies.BackTest(

stock_id="0056",

start_date="2018-01-01",

end_date="2019-01-01",

trader_fund=500000.0,

fee=0.001425,

data_loader=data_loader,

)

obj.stock_price

The backtest will be calculated using the following data

date stock_id Trading_Volume Trading_money open max min close spread Trading_turnover CashEarningsDistribution StockEarningsDistribution

0 2018-01-02 2330 18055269 4188555408 231.5 232.5 231.0 232.5 3.0 9954.0 0.0 0.0

1 2018-01-03 2330 31706091 7504382512 236.0 238.0 235.5 237.0 4.5 13633.0 0.0 0.0

2 2018-01-04 2330 29179613 6963192636 240.0 240.0 236.5 239.5 2.5 10953.0 0.0 0.0

3 2018-01-05 2330 23721255 5681934695 240.0 240.0 238.0 240.0 0.5 8659.0 0.0 0.0

4 2018-01-08 2330 21846692 5281823362 242.0 242.5 240.5 242.0 2.0 10251.0 0.0 0.0

.. ... ... ... ... ... ... ... ... ... ... ... ...

729 2020-12-25 2330 12581145 6449612552 514.0 515.0 510.0 511.0 1.0 14988.0 0.0 0.0

730 2020-12-28 2330 19262886 9890545245 512.0 515.0 509.0 515.0 4.0 16673.0 0.0 0.0

731 2020-12-29 2330 20151736 10370562545 515.0 517.0 513.0 515.0 0.0 17186.0 0.0 0.0

732 2020-12-30 2330 46705107 24306881615 516.0 525.0 514.0 525.0 10.0 33173.0 0.0 0.0

733 2020-12-31 2330 30326332 15989936054 526.0 530.0 524.0 530.0 5.0 25134.0 0.0 0.0

Design Strategy

class ShortSaleMarginPurchaseRatio(Strategy):

"""

summary:

Strategy concept: A higher short-sale-to-margin-purchase ratio means retail investors are bearish.

When institutional investors are net buyers and the stock price tends to rise, we can take the

opposite action of most retail investors by selling, and vice versa.

Strategy rules: short-sale-to-margin-purchase ratio >= 30% and institutional investors net buy, sell

short-sale-to-margin-purchase ratio < 30% and institutional investors net sell, buy

"""

ShortSaleMarginPurchaseTodayRatioThreshold = 0.3

def load_taiwan_stock_margin_purchase_short_sale(self):

self.TaiwanStockMarginPurchaseShortSale = (

self.data_loader.taiwan_stock_margin_purchase_short_sale(

stock_id=self.stock_id,

start_date=self.start_date,

end_date=self.end_date,

)

)

self.TaiwanStockMarginPurchaseShortSale[

["ShortSaleTodayBalance", "MarginPurchaseTodayBalance"]

] = self.TaiwanStockMarginPurchaseShortSale[

["ShortSaleTodayBalance", "MarginPurchaseTodayBalance"]

].astype(

int

)

self.TaiwanStockMarginPurchaseShortSale[

"ShortSaleMarginPurchaseTodayRatio"

] = (

self.TaiwanStockMarginPurchaseShortSale["ShortSaleTodayBalance"]

/ self.TaiwanStockMarginPurchaseShortSale[

"MarginPurchaseTodayBalance"

]

)

def load_institutional_investors_buy_sell(self):

self.InstitutionalInvestorsBuySell = (

self.data_loader.taiwan_stock_institutional_investors(

stock_id=self.stock_id,

start_date=self.start_date,

end_date=self.end_date,

)

)

self.InstitutionalInvestorsBuySell[["sell", "buy"]] = (

self.InstitutionalInvestorsBuySell[["sell", "buy"]]

.fillna(0)

.astype(int)

)

self.InstitutionalInvestorsBuySell = (

self.InstitutionalInvestorsBuySell.groupby(

["date", "stock_id"], as_index=False

).agg({"buy": np.sum, "sell": np.sum})

)

self.InstitutionalInvestorsBuySell["diff"] = (

self.InstitutionalInvestorsBuySell["buy"]

- self.InstitutionalInvestorsBuySell["sell"]

)

def create_trade_sign(self, stock_price: pd.DataFrame) -> pd.DataFrame:

stock_price = stock_price.sort_values("date")

self.load_taiwan_stock_margin_purchase_short_sale()

self.load_institutional_investors_buy_sell()

stock_price = pd.merge(

stock_price,

self.InstitutionalInvestorsBuySell[["stock_id", "date", "diff"]],

on=["stock_id", "date"],

how="left",

).fillna(0)

stock_price = pd.merge(

stock_price,

self.TaiwanStockMarginPurchaseShortSale[

["stock_id", "date", "ShortSaleMarginPurchaseTodayRatio"]

],

on=["stock_id", "date"],

how="left",

).fillna(0)

stock_price.index = range(len(stock_price))

stock_price["signal"] = 0

sell_mask = (

stock_price["ShortSaleMarginPurchaseTodayRatio"]

>= self.ShortSaleMarginPurchaseTodayRatioThreshold

) & (stock_price["diff"] > 0)

stock_price.loc[sell_mask, "signal"] = -1

buy_mask = (

stock_price["ShortSaleMarginPurchaseTodayRatio"]

< self.ShortSaleMarginPurchaseTodayRatioThreshold

) & (stock_price["diff"] < 0)

stock_price.loc[buy_mask, "signal"] = 1

return stock_price

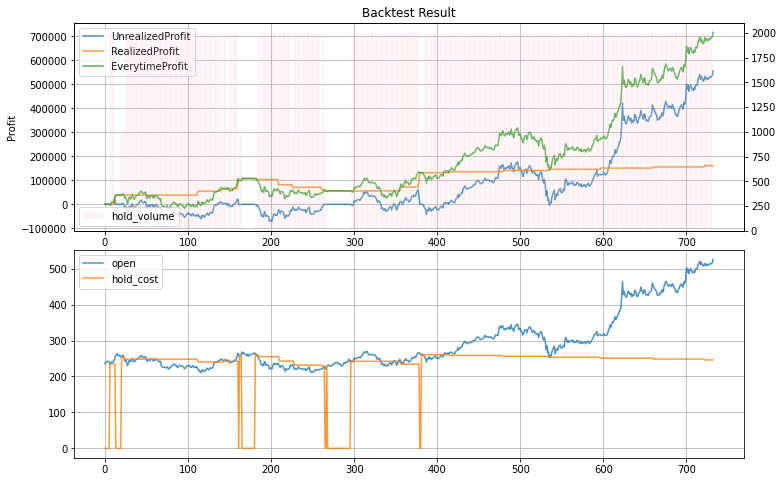

Backtest simulated trading

output

output

stock_id date EverytimeProfit RealizedProfit UnrealizedProfit board_lot hold_cost hold_volume signal tax fee trade_price trader_fund

0 2330 2018-01-03 0.00 0.00 0.00 1000 0.0000 0 0 0.003 0.001425 236.0 500000.000

1 2330 2018-01-04 0.00 0.00 0.00 1000 0.0000 0 0 0.003 0.001425 240.0 500000.000

2 2330 2018-01-05 0.00 0.00 0.00 1000 0.0000 0 0 0.003 0.001425 240.0 500000.000

3 2330 2018-01-08 0.00 0.00 0.00 1000 0.0000 0 -1 0.003 0.001425 242.0 500000.000

4 2330 2018-01-09 0.00 0.00 0.00 1000 0.0000 0 -1 0.003 0.001425 242.0 500000.000

.. ... ... ... ... ... ... ... ... ... ... ... ... ...

728 2330 2020-12-25 692703.01 160992.91 531710.10 1000 245.8705 2000 0 0.003 0.001425 514.0 47251.925

729 2330 2020-12-28 688720.71 160992.91 527727.80 1000 245.8705 2000 0 0.003 0.001425 512.0 47251.925

730 2330 2020-12-29 694694.16 160992.91 533701.25 1000 245.8705 2000 0 0.003 0.001425 515.0 47251.925

731 2330 2020-12-30 696685.31 160992.91 535692.40 1000 245.8705 2000 0 0.003 0.001425 516.0 47251.925

732 2330 2020-12-31 716596.81 160992.91 555603.90 1000 245.8705 2000 0 0.003 0.001425 526.0 47251.925