Backtesting

Online Link¶

The following code shows how to use FinMind to perform strategy backtesting. The backtest is mainly driven by strategies, while DataLoader reads the data provided by FinMind.

When running a backtest, you mainly need to first decide the backtest target, the backtest period, the funding amount, the trading tax, and the design of the strategy.

The backtest logic is mainly to determine the entry, hold, and exit signals. For example:

- If today's calculated signal is -1, it means tomorrow 1 lot of stock will be **sold** at the opening price

- If today's calculated signal is 0, it means do nothing tomorrow

- If today's calculated signal is 1, it means tomorrow 1 lot of stock will be **bought** at the opening price

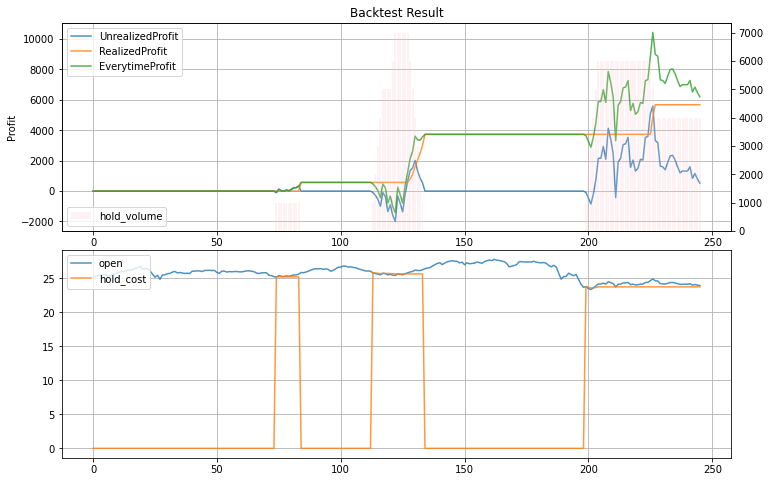

The backtest result provides the following information:

- trade_detail: Detailed backtest data

- compare_market_detail: Trends of cumulative market return and cumulative backtest return

- final_stats: Backtest result

- compare_market_stats: Annualized return of the market and annualized return of the strategy

In the example program, it is mainly divided into using the strategies provided by FinMind and customized strategies.

Initialization: set backtest stock id and time period

import numpy as np

import pandas as pd

from FinMind import strategies

from FinMind.data import DataLoader

from FinMind.strategies.base import Strategy

from ta.momentum import StochasticOscillator

data_loader = DataLoader()

# data_loader.login_by_token(api_token='token') # optional

obj = strategies.BackTest(

stock_id="0056",

start_date="2018-01-01",

end_date="2019-01-01",

trader_fund=500000.0,

fee=0.001425,

data_loader=data_loader,

)

obj.stock_price

The backtest will be calculated using the following data

date stock_id Trading_Volume Trading_money open max min close spread Trading_turnover CashEarningsDistribution StockEarningsDistribution

0 2018-01-02 0056 1868451 46856990 25.00 25.14 25.00 25.13 0.13 733.0 0.0 0.0

1 2018-01-03 0056 3846820 97179269 25.15 25.31 25.15 25.31 0.18 1202.0 0.0 0.0

2 2018-01-04 0056 2736229 69496928 25.31 25.45 25.31 25.41 0.10 957.0 0.0 0.0

3 2018-01-05 0056 2383585 60620826 25.41 25.48 25.39 25.44 0.03 782.0 0.0 0.0

4 2018-01-08 0056 3048596 77817525 25.45 25.57 25.45 25.57 0.13 1236.0 0.0 0.0

.. ... ... ... ... ... ... ... ... ... ... ... ...

242 2018-12-24 0056 1501284 36271556 24.20 24.21 24.09 24.18 0.01 773.0 0.0 0.0

243 2018-12-25 0056 13908880 332473777 24.01 24.06 23.84 23.97 -0.21 6359.0 0.0 0.0

244 2018-12-26 0056 12600245 300239138 24.09 24.09 23.67 23.72 -0.25 6413.0 0.0 0.0

245 2018-12-27 0056 2986526 71566004 24.00 24.02 23.90 23.91 0.19 1651.0 0.0 0.0

246 2018-12-28 0056 2657586 63571334 23.93 23.96 23.89 23.94 0.03 1075.0 0.0 0.0

Design Strategy

class Kd(Strategy):

"""

summary:

Daily KD 80 20

Daily K-line <= 20 enter

Daily K-line >= 80 exit

"""

kdays = 9

kd_upper = 80

kd_lower = 20

def create_trade_sign(self, stock_price: pd.DataFrame) -> pd.DataFrame:

stock_price = stock_price.sort_values("date")

kd = StochasticOscillator(

high=stock_price["max"],

low=stock_price["min"],

close=stock_price["close"],

n=self.kdays,

)

rsv_ = kd.stoch().fillna(50)

_k = np.zeros(stock_price.shape[0])

_d = np.zeros(stock_price.shape[0])

for i, r in enumerate(rsv_):

if i == 0:

_k[i] = 50

_d[i] = 50

else:

_k[i] = _k[i - 1] * 2 / 3 + r / 3

_d[i] = _d[i - 1] * 2 / 3 + _k[i] / 3

stock_price["K"] = _k

stock_price["D"] = _d

stock_price.index = range(len(stock_price))

stock_price["signal"] = 0

stock_price.loc[stock_price["K"] <= self.kd_lower, "signal"] = 1

stock_price.loc[stock_price["K"] >= self.kd_upper, "signal"] = -1

return stock_price

output

output

stock_id date EverytimeProfit RealizedProfit UnrealizedProfit board_lot hold_cost hold_volume signal tax fee trade_price trader_fund

0 0056 2018-01-03 0.00 0.00 0.00 1000 0.000000 0 0 0.001 0.001425 25.15 500000.00000

1 0056 2018-01-04 0.00 0.00 0.00 1000 0.000000 0 0 0.001 0.001425 25.31 500000.00000

2 0056 2018-01-05 0.00 0.00 0.00 1000 0.000000 0 0 0.001 0.001425 25.41 500000.00000

3 0056 2018-01-08 0.00 0.00 0.00 1000 0.000000 0 0 0.001 0.001425 25.45 500000.00000

4 0056 2018-01-09 0.00 0.00 0.00 1000 0.000000 0 0 0.001 0.001425 25.55 500000.00000

.. ... ... ... ... ... ... ... ... ... ... ... ... ...

241 0056 2018-12-24 7274.35 5677.56 1596.79 1000 23.742118 4000 0 0.001 0.001425 24.20 410709.09425

242 0056 2018-12-25 6516.19 5677.56 838.63 1000 23.742118 4000 0 0.001 0.001425 24.01 410709.09425

243 0056 2018-12-26 6835.42 5677.56 1157.86 1000 23.742118 4000 0 0.001 0.001425 24.09 410709.09425

244 0056 2018-12-27 6476.29 5677.56 798.73 1000 23.742118 4000 0 0.001 0.001425 24.00 410709.09425

245 0056 2018-12-28 6196.97 5677.56 519.41 1000 23.742118 4000 0 0.001 0.001425 23.93 410709.09425