回測(引用外部 data)

線上連結¶

初始化,設定回測股票代碼、時間區間

import numpy as np

import pandas as pd

from FinMind import strategies

from FinMind.data import DataLoader

from FinMind.strategies.base import Strategy

from ta.momentum import StochasticOscillator

data_loader = DataLoader()

# data_loader.login_by_token(api_token='token') # 可選

obj = strategies.BackTest(

stock_id="0056",

start_date="2018-01-01",

end_date="2019-01-01",

trader_fund=500000.0,

fee=0.001425,

data_loader=data_loader,

)

obj.stock_price

將會用以下 data 計算回測

date stock_id Trading_Volume Trading_money open max min close spread Trading_turnover CashEarningsDistribution StockEarningsDistribution

0 2018-01-02 2330 18055269 4188555408 231.5 232.5 231.0 232.5 3.0 9954.0 0.0 0.0

1 2018-01-03 2330 31706091 7504382512 236.0 238.0 235.5 237.0 4.5 13633.0 0.0 0.0

2 2018-01-04 2330 29179613 6963192636 240.0 240.0 236.5 239.5 2.5 10953.0 0.0 0.0

3 2018-01-05 2330 23721255 5681934695 240.0 240.0 238.0 240.0 0.5 8659.0 0.0 0.0

4 2018-01-08 2330 21846692 5281823362 242.0 242.5 240.5 242.0 2.0 10251.0 0.0 0.0

.. ... ... ... ... ... ... ... ... ... ... ... ...

729 2020-12-25 2330 12581145 6449612552 514.0 515.0 510.0 511.0 1.0 14988.0 0.0 0.0

730 2020-12-28 2330 19262886 9890545245 512.0 515.0 509.0 515.0 4.0 16673.0 0.0 0.0

731 2020-12-29 2330 20151736 10370562545 515.0 517.0 513.0 515.0 0.0 17186.0 0.0 0.0

732 2020-12-30 2330 46705107 24306881615 516.0 525.0 514.0 525.0 10.0 33173.0 0.0 0.0

733 2020-12-31 2330 30326332 15989936054 526.0 530.0 524.0 530.0 5.0 25134.0 0.0 0.0

設計策略

class ShortSaleMarginPurchaseRatio(Strategy):

"""

summary:

策略概念: 券資比越高代表散戶看空,法人買超股票會上漲,這時候賣可以跟大部分散戶進行相反的操作,反之亦然

策略規則: 券資比>=30% 且法人買超股票, 賣

券資比<30% 且法人賣超股票 買

"""

ShortSaleMarginPurchaseTodayRatioThreshold = 0.3

def load_taiwan_stock_margin_purchase_short_sale(self):

self.TaiwanStockMarginPurchaseShortSale = (

self.data_loader.taiwan_stock_margin_purchase_short_sale(

stock_id=self.stock_id,

start_date=self.start_date,

end_date=self.end_date,

)

)

self.TaiwanStockMarginPurchaseShortSale[

["ShortSaleTodayBalance", "MarginPurchaseTodayBalance"]

] = self.TaiwanStockMarginPurchaseShortSale[

["ShortSaleTodayBalance", "MarginPurchaseTodayBalance"]

].astype(

int

)

self.TaiwanStockMarginPurchaseShortSale[

"ShortSaleMarginPurchaseTodayRatio"

] = (

self.TaiwanStockMarginPurchaseShortSale["ShortSaleTodayBalance"]

/ self.TaiwanStockMarginPurchaseShortSale[

"MarginPurchaseTodayBalance"

]

)

def load_institutional_investors_buy_sell(self):

self.InstitutionalInvestorsBuySell = (

self.data_loader.taiwan_stock_institutional_investors(

stock_id=self.stock_id,

start_date=self.start_date,

end_date=self.end_date,

)

)

self.InstitutionalInvestorsBuySell[["sell", "buy"]] = (

self.InstitutionalInvestorsBuySell[["sell", "buy"]]

.fillna(0)

.astype(int)

)

self.InstitutionalInvestorsBuySell = (

self.InstitutionalInvestorsBuySell.groupby(

["date", "stock_id"], as_index=False

).agg({"buy": np.sum, "sell": np.sum})

)

self.InstitutionalInvestorsBuySell["diff"] = (

self.InstitutionalInvestorsBuySell["buy"]

- self.InstitutionalInvestorsBuySell["sell"]

)

def create_trade_sign(self, stock_price: pd.DataFrame) -> pd.DataFrame:

stock_price = stock_price.sort_values("date")

self.load_taiwan_stock_margin_purchase_short_sale()

self.load_institutional_investors_buy_sell()

stock_price = pd.merge(

stock_price,

self.InstitutionalInvestorsBuySell[["stock_id", "date", "diff"]],

on=["stock_id", "date"],

how="left",

).fillna(0)

stock_price = pd.merge(

stock_price,

self.TaiwanStockMarginPurchaseShortSale[

["stock_id", "date", "ShortSaleMarginPurchaseTodayRatio"]

],

on=["stock_id", "date"],

how="left",

).fillna(0)

stock_price.index = range(len(stock_price))

stock_price["signal"] = 0

sell_mask = (

stock_price["ShortSaleMarginPurchaseTodayRatio"]

>= self.ShortSaleMarginPurchaseTodayRatioThreshold

) & (stock_price["diff"] > 0)

stock_price.loc[sell_mask, "signal"] = -1

buy_mask = (

stock_price["ShortSaleMarginPurchaseTodayRatio"]

< self.ShortSaleMarginPurchaseTodayRatioThreshold

) & (stock_price["diff"] < 0)

stock_price.loc[buy_mask, "signal"] = 1

return stock_price

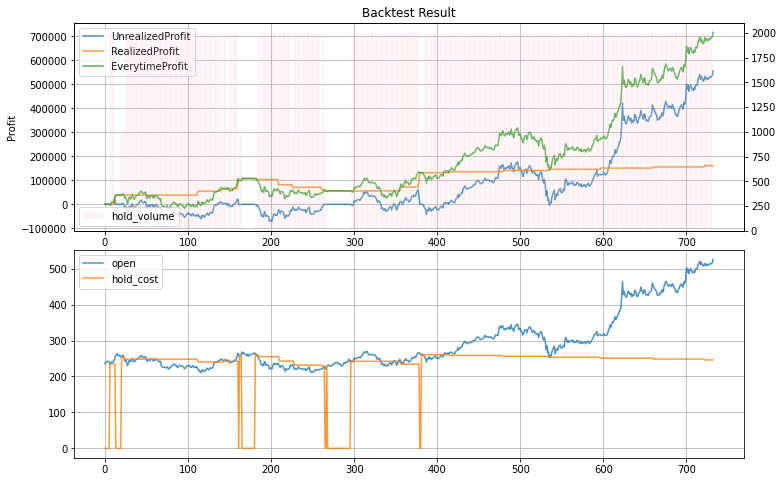

output

output

stock_id date EverytimeProfit RealizedProfit UnrealizedProfit board_lot hold_cost hold_volume signal tax fee trade_price trader_fund

0 2330 2018-01-03 0.00 0.00 0.00 1000 0.0000 0 0 0.003 0.001425 236.0 500000.000

1 2330 2018-01-04 0.00 0.00 0.00 1000 0.0000 0 0 0.003 0.001425 240.0 500000.000

2 2330 2018-01-05 0.00 0.00 0.00 1000 0.0000 0 0 0.003 0.001425 240.0 500000.000

3 2330 2018-01-08 0.00 0.00 0.00 1000 0.0000 0 -1 0.003 0.001425 242.0 500000.000

4 2330 2018-01-09 0.00 0.00 0.00 1000 0.0000 0 -1 0.003 0.001425 242.0 500000.000

.. ... ... ... ... ... ... ... ... ... ... ... ... ...

728 2330 2020-12-25 692703.01 160992.91 531710.10 1000 245.8705 2000 0 0.003 0.001425 514.0 47251.925

729 2330 2020-12-28 688720.71 160992.91 527727.80 1000 245.8705 2000 0 0.003 0.001425 512.0 47251.925

730 2330 2020-12-29 694694.16 160992.91 533701.25 1000 245.8705 2000 0 0.003 0.001425 515.0 47251.925

731 2330 2020-12-30 696685.31 160992.91 535692.40 1000 245.8705 2000 0 0.003 0.001425 516.0 47251.925

732 2330 2020-12-31 716596.81 160992.91 555603.90 1000 245.8705 2000 0 0.003 0.001425 526.0 47251.925